We put the right combination of financial tools and top-rated personal service together to meet your individual mortgage needs. Learn how we can help you fulfill your homeownership goals.

About Silverton

Founded in 1998, Silverton Mortgage is an acknowledged industry leader within the mortgage community. We’ve always believed that maintaining the entire loan process in-house keeps everyone involved: borrower, real estate agent, and Silverton Mortgage. One team, one goal.

Because of our collaborative culture, we are honored to continually be recognized with the industry’s leading customer satisfaction rankings and stunning growth as we continually expand our lending footprint.

Success is always a team effort. At Silverton Mortgage, we credit our years of success to the trust of our clients and the hard work of the talented individuals on our team.

Who We Are

What We Offer

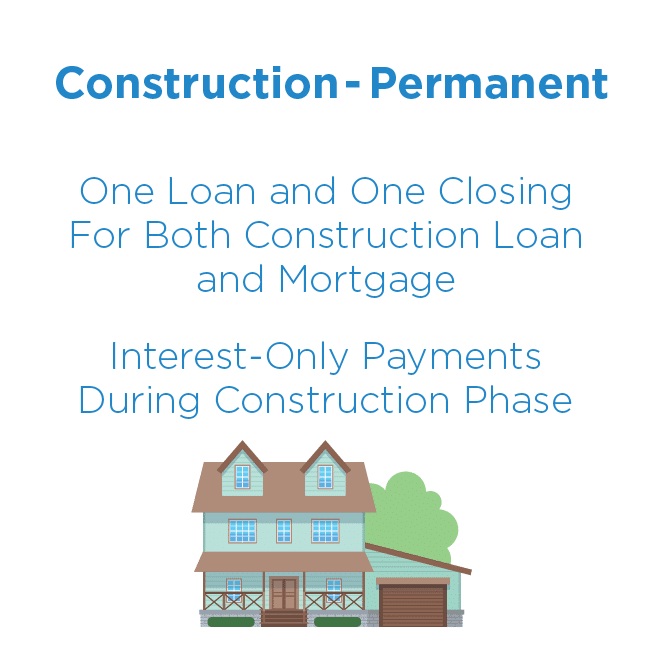

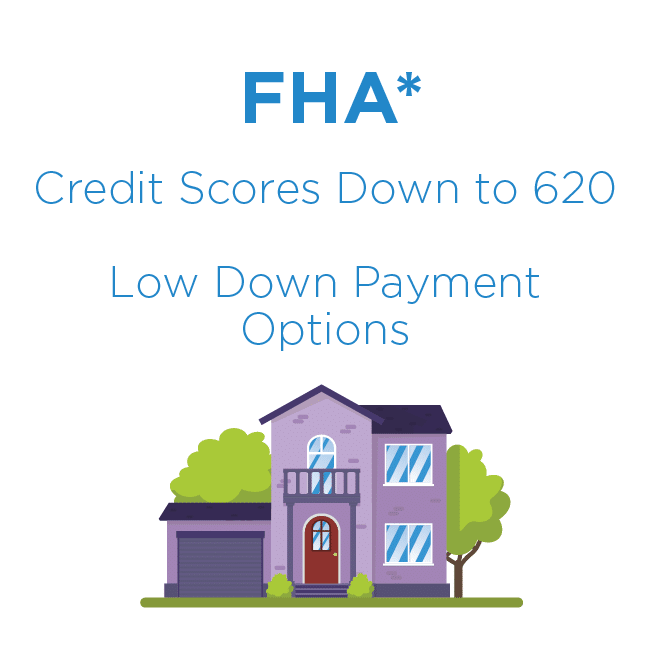

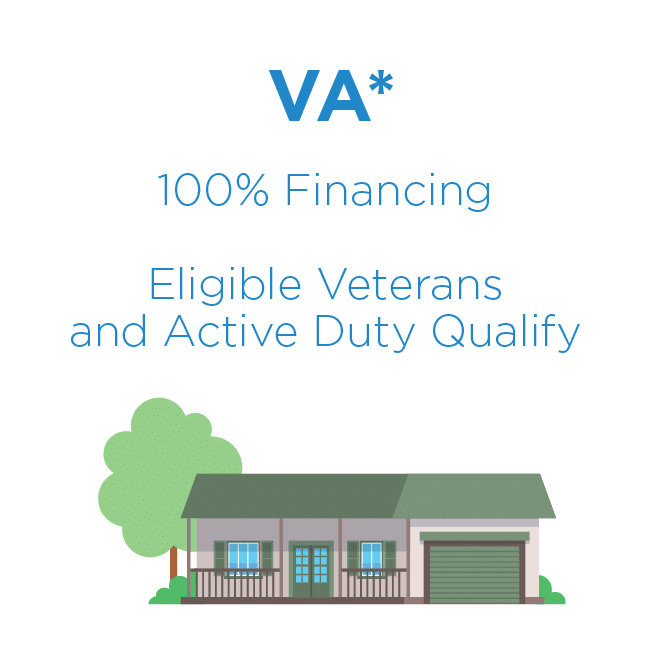

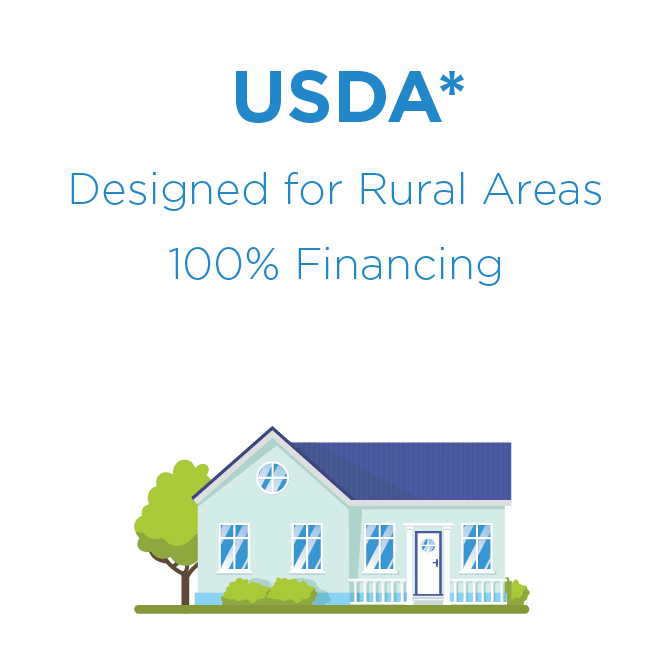

Our Loan Originators are trained to walk borrowers through several different loan types, including:

Going Above and Beyond

Silverton Mortgage is dedicated to giving back to its communities, as illustrated by its motto: Success without sharing is failure. In 2012, Silverton Mortgage President Josh Moffitt founded The Silverton Foundation, which provides mortgage and rent assistance for families struggling with financial hardship due to their child’s serious illness. Silverton Mortgage donates to the Foundation on behalf of its new homeowners.

Start Today!

Whether you’re a first-time homebuyer, in market for your forever home, or anywhere in between, our staff is here to help you get there. Fill out the Contact Us form to start the conversation towards homeownership!